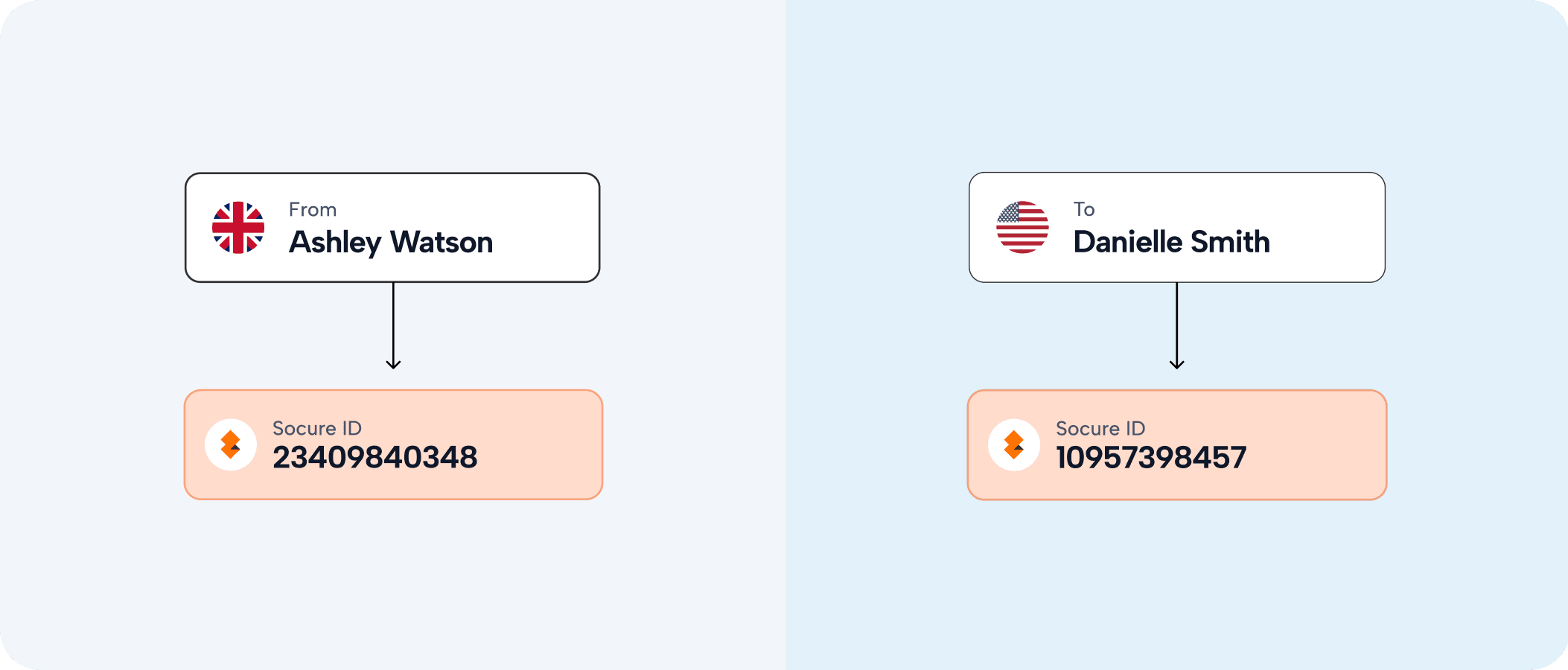

Payment Screening

Screen senders, beneficiaries, bank accounts and crypto addresses for sanctions risk in a single API call.

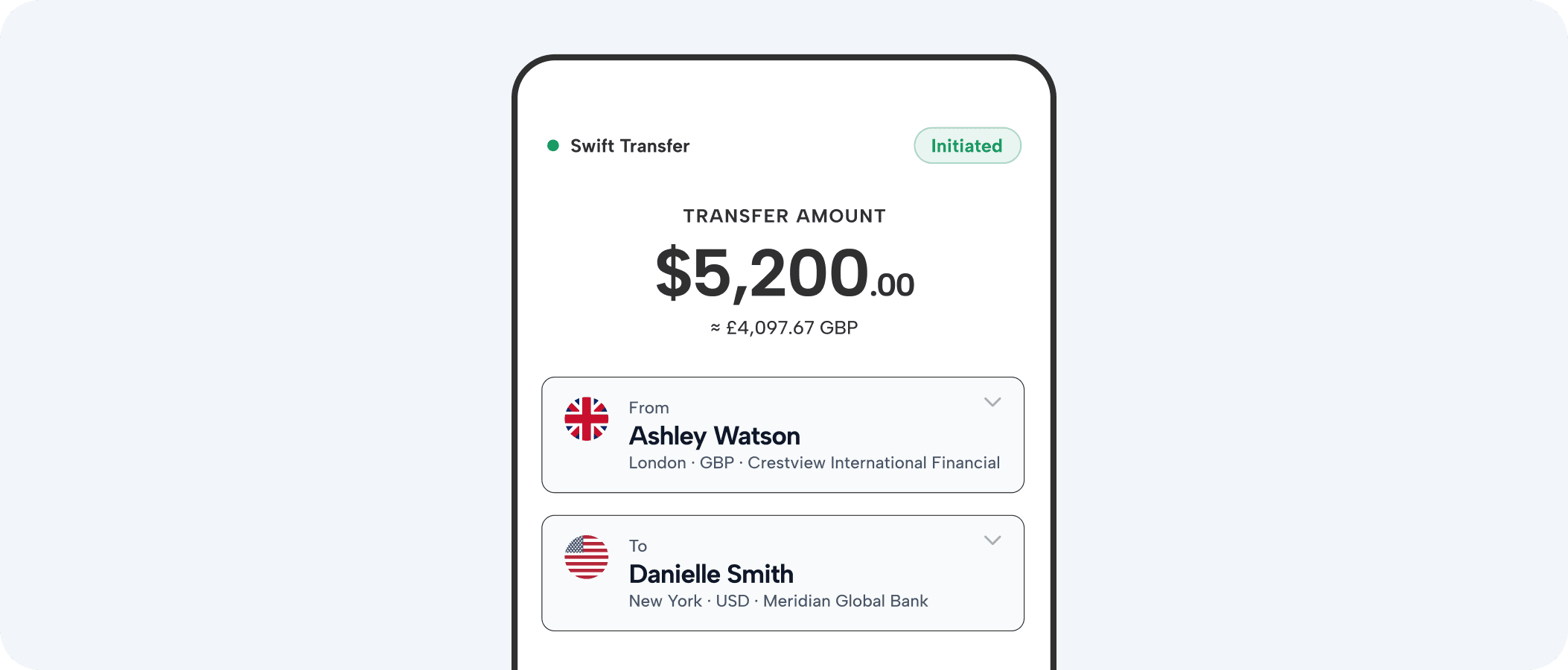

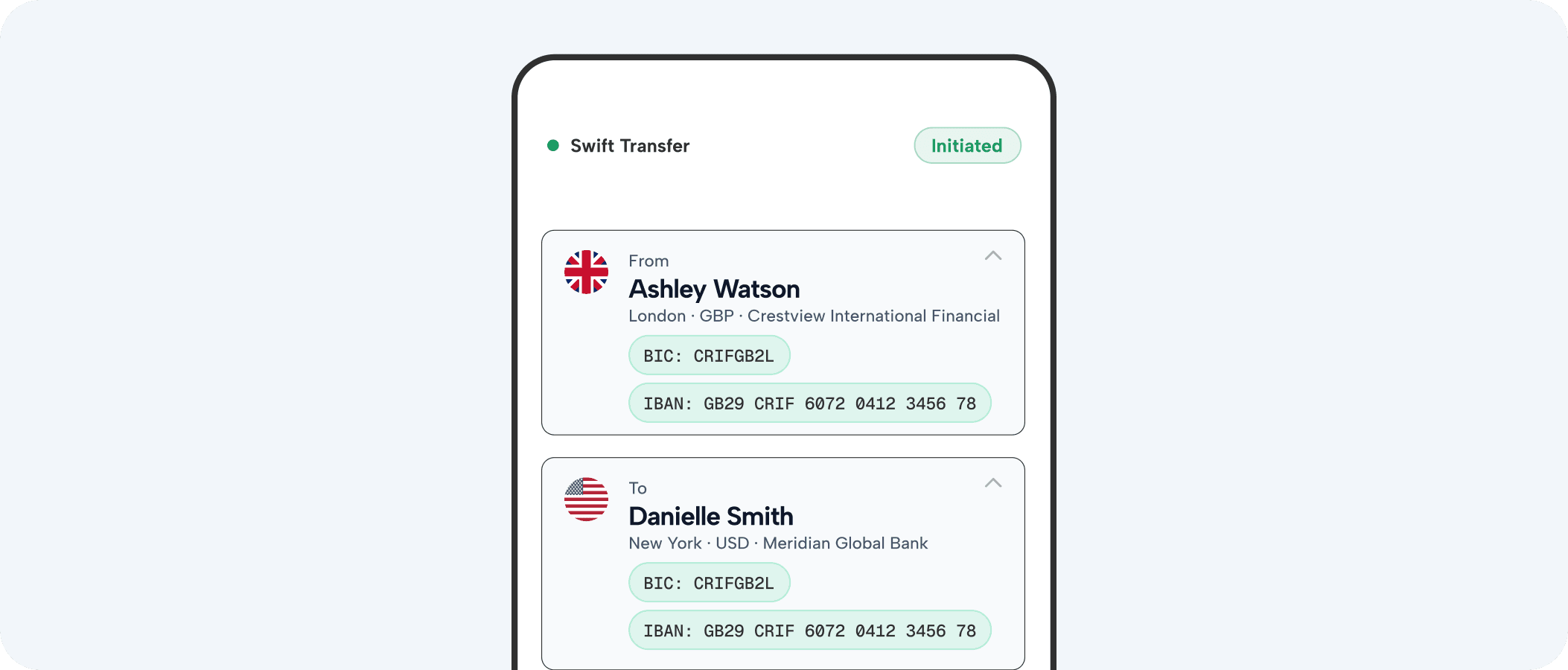

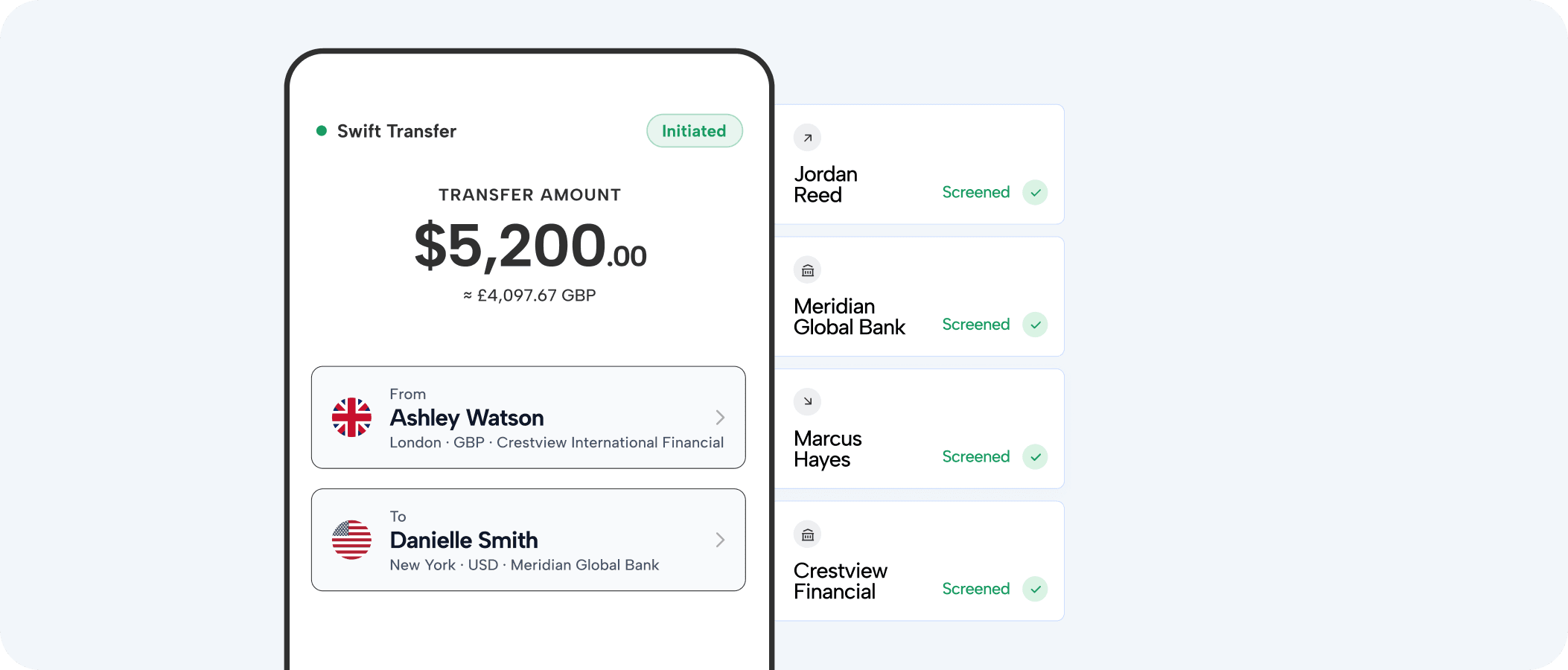

Screen all payment participants with one API call.

Delivering identity intelligence for every payment participant without the latency and complexity of legacy multi-call approaches. Socure’s single API architecture simplifies routing logic while keeping policies consistent across every payment, reducing friction without sacrificing compliance.

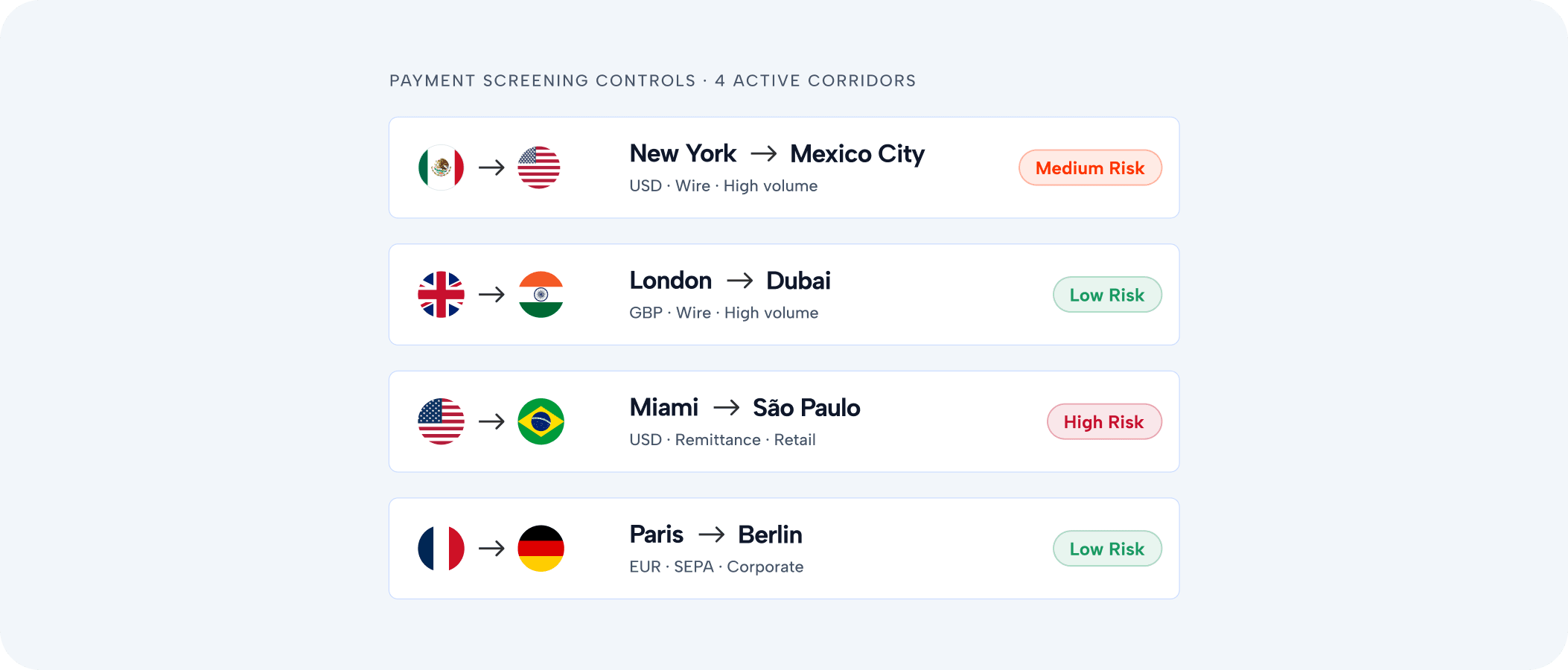

Our smarter screening goes beyond name matching to truly understand identity. Granular, flexible controls replace blanket policies, giving you unmatched accuracy and adaptability across every corridor, payment type, and regulatory requirement.

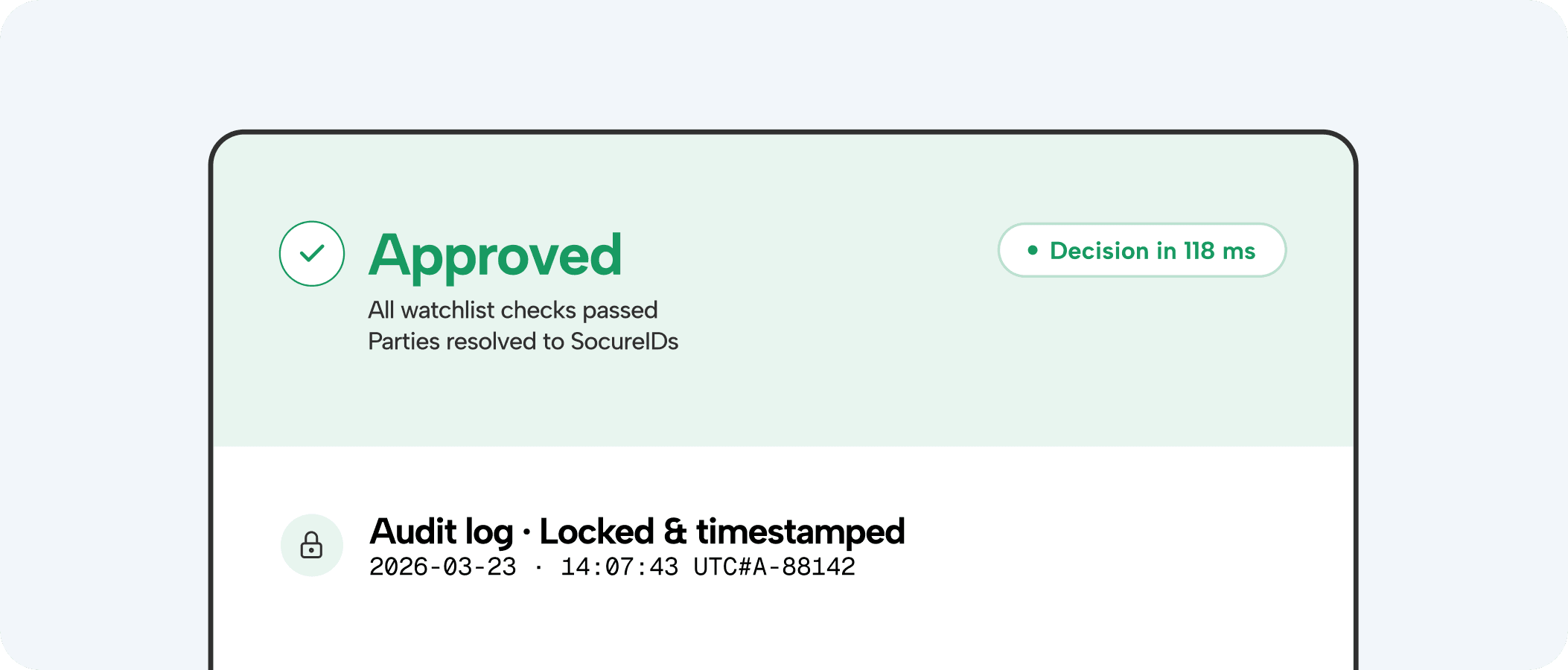

The single-API decision layer for payment screening.

Manage granular screening controls for each use case and jurisdiction

Select sanctions lists, set matching thresholds, apply country or date of birth filters granularly for each jurisdiction, risk segment, product line and more, for seamless, global compliance at scale.

AI Case Analyst

Reduce case review time by up to 80% using AI-generated summaries, explanations, and recommendations to accelerate watchlist and payment screening investigations while maintaining full control and a clear, auditable decision trail.